Low-cost grain drags down Italian pasta prices

15 October 2016Record harvest in Italy, a leap in 2016 to the best results in 10 years. But the drop in quality is worrying.

by Centro studi economici Pastaria

The costs – at least their variable part – will almost certainly have a positive impact on company accounts. But it is a question of assessing whether the savings, that Italian manufacturers will be able to make by stocking up on grain and flour at this year’s decidedly more advantageous prices, will lead to an effective increase in profitability in the months to come.

The most recent evidence says that although, on the one hand, Italian companies can purchase on the grain market at prices up to 30-40% lower than those of last year (with two-figure reductions also on the semolina flour market), the other side of the coin is that requests for discounts are already coming in from buyers and large scale distribution.

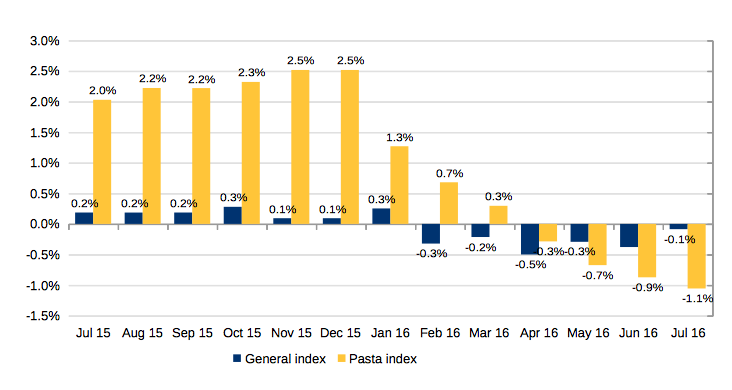

However, it is not surprising to note that retail prices, those paid by consumers, have inverted in the last four months the upward tendency which had reached its peak in December, with an annual +2.5%.

In July of this year, registers ISTAT (National Statistics Institute), pasta retail prices were seen to have dropped by 1.1%, the strongest downward trend since November 2010.

This tendency will continue also in the months to come, and may most likely even intensify, incorporating in consumer prices the deflationary components that have been characterizing the (agricultural and industrial) production phases for some time now, upstream of the distribution phases.

There are good possibilities that the drop in prices could, if nothing else, contribute to curbing the downward dynamics of pasta consumption, which remained in the negative in the first six months of 2016 as well.

In contrast, on the exportation front, it might well be possible to make up the volumes lost over the last twelve months, even with slightly lower sales figures.

Although last year’s pasta exports experienced a drastic about-face, losing 6 percentage points in terms of physical data, this year the dynamics could change direction with crucial results. In five months, from January to May 2016, a fractional recovery could already be seen that marked the trend reversal long-awaited by the operators.

Moreover, the discount policy, facilitated by the cut in production costs, might also be able to improve competitiveness abroad and, above all, consolidate market shares, not only in traditional markets but also in emerging ones. [hidepost]

This would also be an important sign of a change in direction, in a sector in which Italy is absolute leader on a worldwide scale, even although it is facing growing pressure from the competition presented by the new producing countries.

Prospects are less favourable as regards sales figures. The possibility of repeating the positive performance of last year (+6%) appears highly unlikely under the current circumstances. It would already be an excellent result if revenues were to maintain the levels of 2015, but in this case the drop in prices would have to be re-absorbed by an increase in the volumes exported.

Export developments up to and throughout the month of May represent, for the time being, a reversal of the trend in foreign sales which, one year on, has shown a reduction of 3%.

With regard to the harvests, the outlines of the (still provisional) budget for the new production year are becoming clearer. A season marked, in Italy, by a production boom, with the estimates of Italmopa (the association that represents the flour milling sector) recording production at 5.5 million tonnes, the highest level obtained in the last ten years.

Opinions on the technical characteristics are less generous. Although the volumes are more than satisfactory, the situation appears severely undermined in terms of quality, particularly in Apulia where, in many cases, the repeated rain and excessive humidity during harvest time resulted in a reduction in the protein content of the grain.

Production has also been abundant in North America this year. Canada, with a 15% increase compared to the last season, allegedly achieved a harvest of 6.2 million tonnes of durum wheat, according to the calculations of the Department of Agriculture of Ottawa. Forecasts are also positive for exports and stocks, assessed on volumes that are higher, by 11% and 30% respectively, than last year.

Also for grain shipped from Canadian ports FOB prices dropped substantially this summer. At the end of August, the futures contract on the first delivery to the ICE of London – the reference stock exchange for agricultural commodities – closed with an annual shortfall of 20%, although in anticipation of a high demand from the countries of North Africa, an area in which the harvests were poor.

[/hidepost]

Keep reading, download the magazine

PASTARIA INTERNATIONAL 5/2016 (ENGLISH) (high resolution PDF) (91.0 MiB, 1,286 download)

PASTARIA INTERNATIONAL 5/2016 (ENGLISH) (high resolution PDF) (91.0 MiB, 1,286 download)

Registrazione necessaria. Sign-up to download.

PASTARIA INTERNATIONAL 5/2016 (ENGLISH) (low resolution PDF) (13.7 MiB, 2,129 download)

Registrazione necessaria. Sign-up to download.

PASTARIA INTERNATIONAL 5/2016 (ENGLISH) (file iBooks) (95.3 MiB, 2,837 hits)

PASTARIA INTERNATIONAL 5/2016 (ENGLISH) (file iBooks) (95.3 MiB, 2,837 hits)

SPIRALI PER SURGELAZIONE

0,00 €

SPIRALI DI TRASPORTO

0,00 €